transportation

Transportation: Air and Train Travel

Summary

This collection of data includes the following indicators:

AIR TRAVEL

revenue passenger miles, 2014-2040 & 2014-2034, US Energy Information Administration (EIA), Boeing

seat miles demanded by plane size, 2014-2040, EIA

annual passengers on US-based flights, 2003-2015, Dept. of Transportation (DoT)

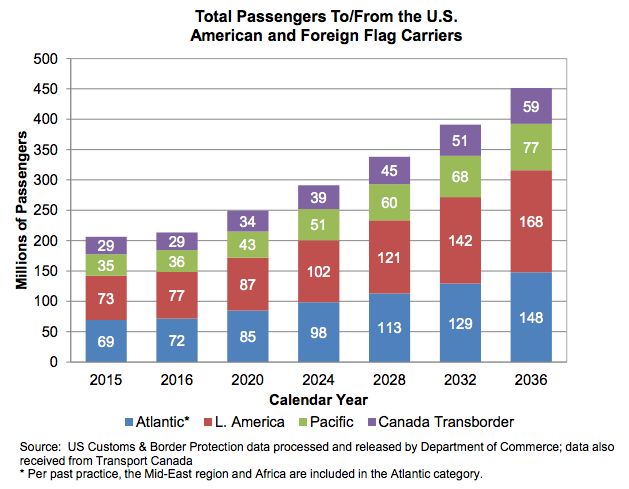

annual passengers to/from the US, 2015-2036, FAA

passengers to/from/within the US CAGR, 2014-2034, IATA

number of aircraft by type, 1965-2014, DoT

number of certificated aircraft, 1960-2005, Statista (citing AIA, DoT, FAA)

number of commercial aircraft by size, 2006-2036 & 2014/2034, FAA, Boeing

number of general aircraft by size, 2006-2036, FAA

number of airlines, [forthcoming data] & 1950/2002 & speculation, DoT, Aviation Mgmt College, Boeing

number of airports, 1980-2014 & current count by size, DoT, FAA

incoming intl travel and “mega-cities”, 2012/2032, Airbus

PERSONAL DRONES

consumer drone market USD millions, 2013-2024, Grand View Research

RAIL TRAVEL

passenger miles light rail and heavy rail, 1980-2014, DoT

passenger miles commuter rail and Amtrak, 1960-2014, DoT

miles of subway trackway, 1997-2014, DoT

high speed rail development map, 2015-2030 & undated, US High Speed Rail Association, DoT

Findings

Miles Flown

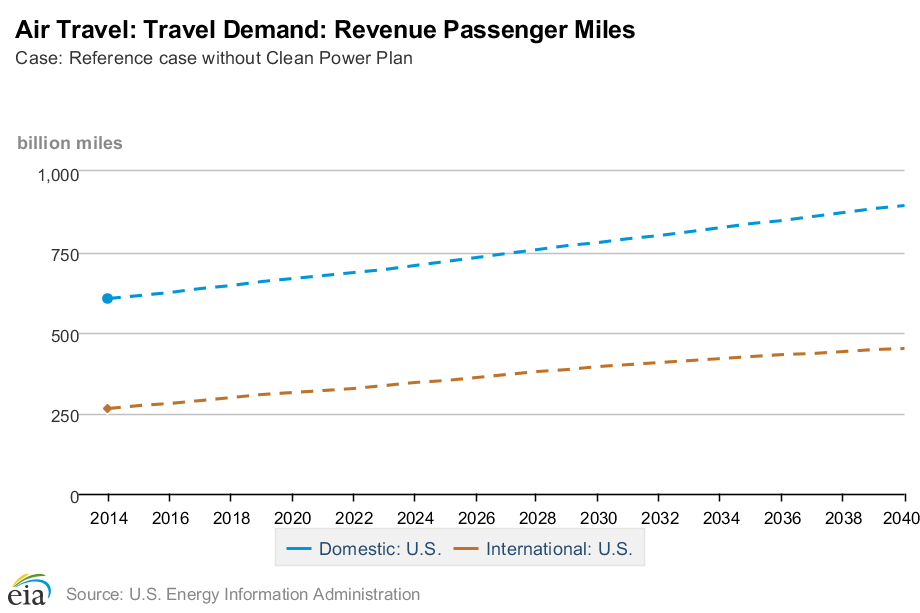

Travel Demand — Revenue Passenger Miles (billion miles)

Note: Revenue revenue passenger miles are calculated by multiplying the number of revenue paying-passengers aboard the vehicle by the distance traveled. Sometimes abbreviated to RPM or RPK.

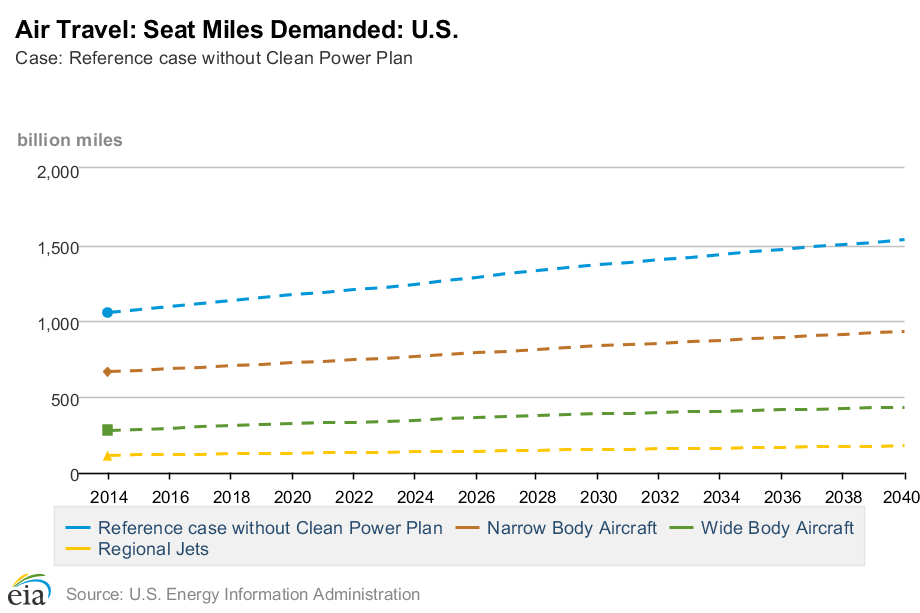

Seat Miles Demanded (total and by plane size)

src:

US Energy Information Administration. 2016.

“Annual Energy Outlook 2016”

Transportation Sector

Table: Air Travel Energy Use

NOTE: ONLY THE DATA TABLES ARE CURRENTLY AVAILABLE. THE EXECUTIVE SUMMARY AND OTHER NARRATIVE PARTS OF THE REPORT WILL BE AVAILABLE AFTER JULY 21, 2016. CHECK BACK HERE.

*

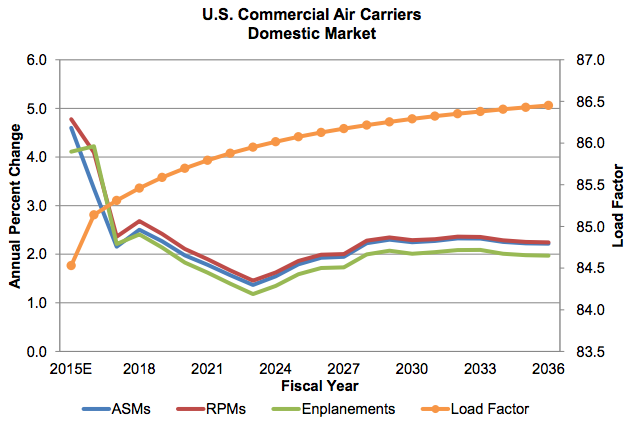

“Owing to network carrier capacity discipline, we think that the domestic US market is ripe for even higher growth than previously forecast. Our revised domestic forecast has traffic growth in the range of 2.5 to 3.0 percent over the next five years. With a load factor of 83 percent for 2014 (and average load factors in excess of 80 percent over the past few years), network carriers may be prompted to further ease their capacity discipline in the face of competitive pressures and continued economic recovery.”

src:

Boeing. 2015.

“Current Market Outlook: 2015–2034.” P. 23, 42.

contact: BoeingCurrentMarketOutlook@Boeing.com

Passengers Flying

The U.S. Department of Transportation’s Bureau of Transportation Statistics (BTS) reported today that U.S. airlines and foreign airlines serving the United States carried an all-time high of 895.5 million systemwide (domestic and international) scheduled service passengers in 2015, 5.0 percent more than the previous record high of 853.1 million reached in 2014. The systemwide increase was the result of a 5.0 percent rise from 2014 in the number of passengers on domestic flights (696.2 million in 2015) and 4.7 percent growth from 2014 in passengers on U.S. and foreign airlines’ flights to and from the U.S. (199.4 million in 2015)

Annual Total Passengers on US-Based Flights

Data available from the source (table, or excel)

src:

Department of Transportation. March 2016.

“2015 U.S.-Based Airline Traffic Data.”

Bureau of Transportation Statistics.

media contact: Dave Smallen, 202-366-5568

TO DO: SEE IF THE DEPT. OF TRANSPORTATION HAS OLDER FIGURES.

*

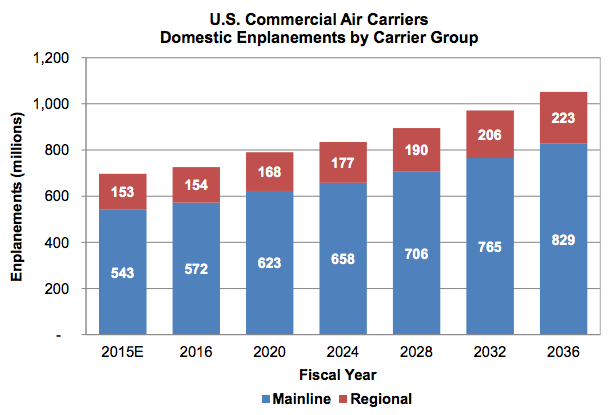

Enplanements = passengers

Note: Mainline carriers are defined as those providing service primarily via aircraft with 90 or more seats. Regionals are defined as those providing service primarily via aircraft with 89 or less seats and whose routes serve mainly as feeders to the mainline carriers.

src:

Federal Aviation Administration. Accessed July 1, 2016.

“FAA Aerospace Forecast: Fiscal years 2016-2036.”

*

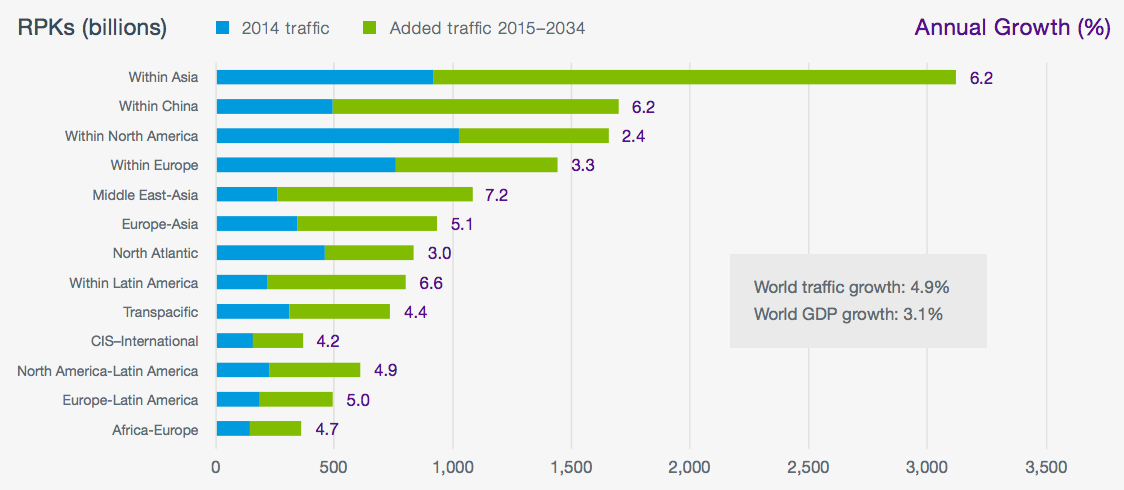

Traffic to, from and within the US is expected to grow at an average annual growth rate of 3.2% that will see 1.2 billion passengers by 2034 (559 million more than 2014).

src:

IATA. October 2014.

“New IATA Passenger Forecast Reveals Fast-Growing Markets of the Future.”

TO DO: INQUIRE ABOUT NEWER FORECAST

David Oxley, IATA Senior Economist, oxleyd@iata.org

OR corpcomms@iata.org

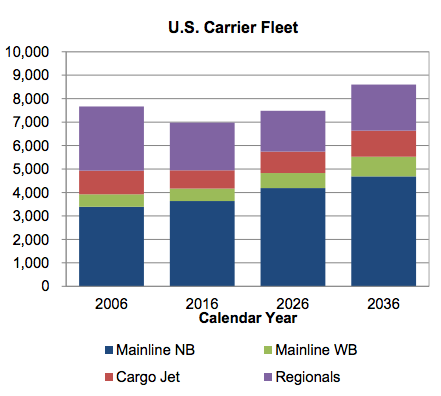

Number and Types of Commercial Jets

Table 1-13: Active U.S. Air Carrier and General Aviation Fleet by Type of Aircraft (Number of carriers)

Annual data available 1965-2014

src:

US Department of Transportation. Accessed July 1, 2016.

“Table 1-13: Active U.S. Air Carrier and General Aviation Fleet by Type of Aircraft (Number of carriers).”

TO DO: PULL DATA OUT INTO A GOOGLE SPREADSHEET

*

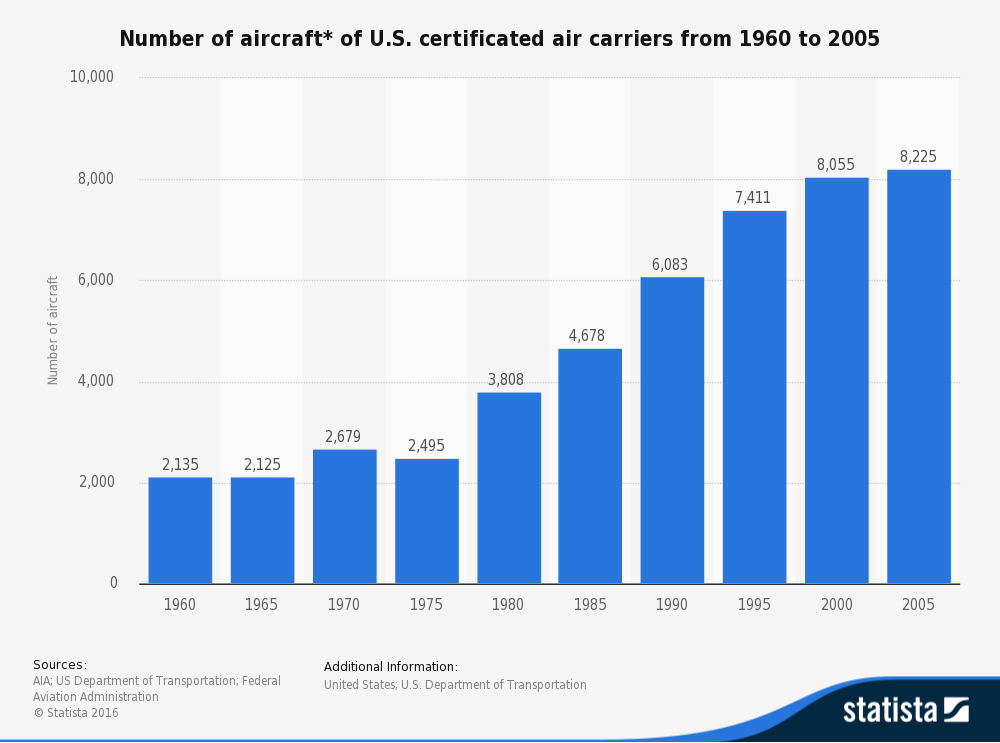

Number of aircraft of U.S. certificated air carriers from 1960 to 2005

The timeline shows the number of U.S. certificated air carrier aircraft from 1960 to 2005. In 2000, there were 8,055 certificated air carrier aircraft in the United States.

src:

Statistia. Accessed July 8, 2016.

“Number of aircraft* of U.S. certificated air carriers from 1960 to 2005.”

citing:

AIA; Dept. of Transportation; Federal Aviation Administration

FORECAST BELOW

*

US Commercial Aircraft Forecast

(CC’s notes: includes scheduled air services – pilot is paid, must have commercial pilot certificate)

The number of aircraft in the U.S. commercial fleet is forecast to increase from 6,871 in 2015 to 8,414 in 2036, an average annual growth rate of 1.0 percent a year. Increased demand for air travel and growth in air cargo is expected to fuel increases in both the passenger and cargo fleets.

NB: narrow-body

WB: wide-body

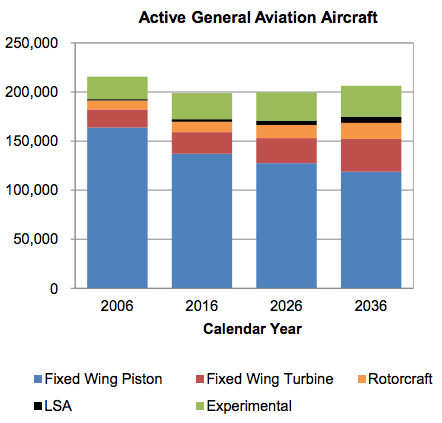

General Aviation Forecast

(CC’s notes: does not include schedule air services – pilot not paid, private pilot certificate is sufficient)

The active general aviation fleet is projected to increase at an average annual rate of 0.2 percent over the 21-year forecast period, growing from an estimated 203,880 in 2015 to 210,695 aircraft by 2036.

LSA: light-sport-aircraft (category established in 2005)

Note: An active aircraft is one that flies at least one hour during the year.

src:

Federal Aviation Administration. Accessed July 1, 2016.

“FAA Aerospace Forecast: Fiscal years 2016-2036.”

*

src:

Boeing. 2015.

“Current Market Outlook: 2015–2034.” p.42

contact: BoeingCurrentMarketOutlook@Boeing.com

Number of Airlines

The Dept. of Transportation has a simple PDF list of certificated air carriers and commuter air carriers, but there’s no “member since” info and presumably doesn’t include former members.

https://www.transportation.gov/policy/aviation-policy/certificated-air-carriers-list

https://www.transportation.gov/policy/aviation-policy/commuter-air-carriers-list

https://www.transportation.gov/policy/aviation-policy/licensing/US-carriers

Air Carrier Fitness Division

Office of Aviation Analysis

Dept. of Transportation

1200 New Jersey Ave, SE

Washington, DC 20590

United States

Phone: (202) 366-9721

Business Hours:

8:30am-5:00pm ET, M-F

EMAILED LAURALYN REMO, laura.remo@dot.gov, JULY 8, 2016.

Caitlin Harvey, caitlin.harvey@dot.gov, wrote back and shared the following Excel files (with data from 1978-2016):

“Commuter Carrier List.xls”

“Certificated Carrier List.xls”

*

Certificated airlines in the US

1950 – 17 airlines

2002 – 12 airlines

src:

Aviation Management College.

“Introduction to Aviation Economics.”

Slide 15.

*

“Post the 2008 downturn, the introduction of the ultra-low-cost carrier (ULCC) business model in the United States is literally taking off. Spirit Airlines is the fastest growing domestic airline, recording double-digit growth. Frontier Airlines, which is undergoing a change in strategy, is expected to challenge Spirit in the quest to become the preeminent ULCC in the United States. The expectation is that over time, the industry will further consolidate, with the LCC and smaller network carriers becoming potential consolidation targets.”

[emphasis mine]

src:

Boeing. 2015.

“Current Market Outlook: 2015–2034.” P.42

contact: BoeingCurrentMarketOutlook@Boeing.com

Number of Airports

Table 1-3: Number of U.S. Airports

Annual data available 1980-2014

src:

US Department of Transportation. Accessed July 6, 2016.

“Table 1-3: Number of U.S. Airports.”

NOTE: THESE FIGURES ARE MUCH HIGHER THAN THOSE BELOW DESCRIBING THE NUMBER OF US AIRPORTS WHERE REGIONAL AIRLINES OPERATE. THOSE FIGS MIGHT BE REFERRING TO “CERTIFICATED” AIRPORTS, BUT DATA FOR THESE AIRPORTS ARE ONLY AVAILABLE 1994-2004.

TO DO: PULL DATA OUT INTO A GOOGLE SPREADSHEET

*

A total of 614 U.S. airports are served by regional airlines, with 70% (431 airports) relying exclusively on regional airlines for their scheduled service.

The United States’ air transportation network is the most developed in the world, but is evolving as airlines battle rising costs. While regional aircraft operate approximately 33% of commercial flights worldwide, 50% of all commercial flights in the United States are flown by regional aircraft with less than 100 seats. According to the Regional Airline Association (RAA), average capacity of U.S. regional aircraft has increased from 37 seats in 2000 to 50 seats in 2005 and to 56 seats in 2013. Average trip length increased from 476 kilometres in 2000 to 763 kilometres in 2013. These trends are expected to continue as new large regional aircraft replace 20-to59-seat aircraft.

src:

Bombardier. July 2014.

“Bombardier Commercial Aircraft Market Forecast 2014-2033.”

P.31

citing:

Regional Airline Association (RAA)

*

2014

Total FAA Towers – 264

Total Contract Towers – 252

2014 airport hubs

30 large hub airports (1%+ total US passenger enplanements)

31 medium hub airports (.25-.99%)

74 small hub airports (.05-.249%)

381 non-hub airports non-hub airports (less than .05%)

Total: 516

For example, Atlanta was the busiest large hub in 2014, and it saw 6.13% of total US enplanements in 2014.

Enplanements at large hubs expected to increase at an annual rate of 2.0% through 2040. Operations (take-offs and landings) at these hubs are forecast to increase at an annual rate of 1.6%.

Medium and small hubs are forecast to increase at 2.0% and 1.7% annually, respectively. Operations at medium hubs expected to grow at 1.3% annually. Operations at small hubs are forecast to grow at .8% per year.

Non-hub operations accounted for 52% of total operations at FAA and Federal contract towers. General aviation operations (e.g.: private) accounted for the majority of operations at these smaller airports.

src:

Federal Aviation Administration. 2015.

“Terminal Area Forecast Summary: Fiscal Years 2015-2040.”

contact:

Roger Schaufele, Jr.

Manager

Forecast and Performance Analysis Division

Office of Aviation Policy and Plans

202-267-3306

Roger.Schaufele@faa.gov

EMAILED ROGER SHAUFELE JULY 8, 2016.

ALSO TRY CONTACTING THE FAA OFFICE OF THE ASSOCIATE ADMIN FOR AIRPORTS. NO EMAIL, PHONE IS DISCONNECTED.

*

Airport Data retrieval form from the FAA.

TO DO: CONTACT FAA FOR AN ANNUAL TALLY. NOT SURE BEST CONTACT AVENUE.

TRY THE FORM HERE. OR THE OFFICE OF THE ASSOCIATE ADMIN FOR AIRPORTS

Incoming Intl Travel to US

In 2012, the US has one “aviation mega-city” receiving more than 50,000 daily long-haul passengers. In 2032, there will be five.

Long haul traffic: flight distance >2,000nm, excl. domestic traffic

citing: GMF 2013; Cities with more than 10,000 daily passengers

src:

Bob Lange. September 2013.

“Global Market Forecast 2013-2032.”

Airbus. P. 15, 29

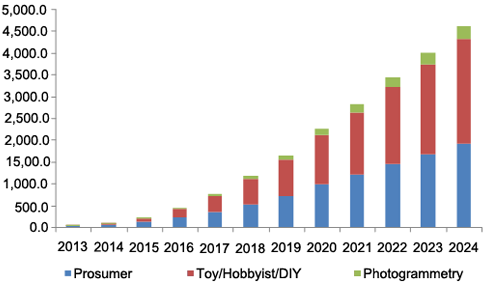

Personal Drones

Grand View Research is tracking the consumer drone market, and although the summary for their recent report does not include much unit data, the forecast does show the relative growth across three consumer applications: prosumer, toy/hobbyist/DYI, and photogrammetry.

North America consumer drone market by technology, 2012 – 2022 [sic] (USD Million)

src:

Grand View Research. May 2016.

“Consumer Drone Market Analysis By Product (Multi-Rotor, Nano), By Application (Prosumer, Toy/Hobbyist, Photogrammetry) And Segment Forecasts To 2024.”

Rail Passenger Miles

Table 1-40: U.S. Passenger-Miles (Millions)

Includes

Light rail: 1980-2014

Heavy rail: 1980-2014

Commuter rail: 1960-2014

Intercity/Amtrak: 1960-2014

Note: This table also includes figures for air, highway, bus and ferry travel.

src:

US Department of Transportation. Accessed July 11, 2016.

“Table 1-40: U.S. Passenger-Miles (Millions).”

TO DO: PULL DATA OUT INTO A GOOGLE SPREADSHEET

Definitions src

Heavy Rail: includes subways, elevated railways, and metropolitan (metro) railways and refers to an electric railway with the capacity to transport a heavy volume of passenger traffic and characterized by exclusive rights-of-way, multicar trains, high speed, rapid acceleration, sophisticated signaling, and high-platform loading.

Light Rail: A streetcar-type vehicle operated on city streets, semiexclusive rights-of-way, or exclusive rights-of-way. Service may be provided by step-entry vehicles or by level boarding.

Commuter Rail: Urban passenger train service for short-distance travel between a central city and adjacent suburb. Does not include rapid rail transit or light rail service.

Amtrak: Operated by the National Railroad Passenger Corporation of Washington, D.C., this rail system was created by the Rail Passenger Service Act of 1970 (P.L. 91-518, 84 Stat. 1327) and given the responsibility for the operation of intercity, as distinct from suburban, passenger trains between points designated by the Secretary of Transportation.

Miles of Trackway

Subway: 1997-2014 (in separate annual reports)

src:

US Department of Transportation ~1997-2014.

“NTD Data Reports.”

Federal Transit Administration.

TO DO: EXTRACT DATA

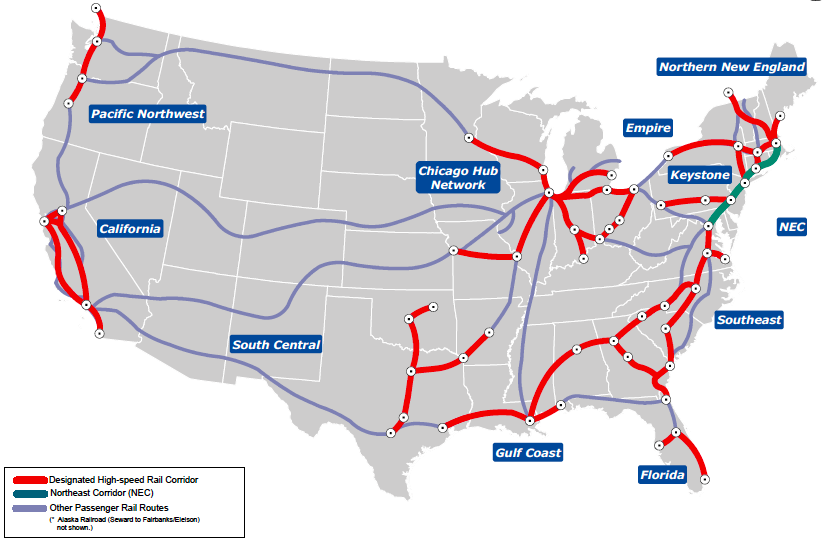

High-Speed Rail

The High Speed Rail Association has published a US network phasing plan showing construction phases from 2015-2030.

src:

US High Speed Rail Association. Accessed July 11, 2016.

“US HSR Network Phasing Plan.”

NOTE: This plan may reflect expect START dates for construction, rather than completion. For example, while work on phase 1 of California’s high-speed rail system began in 2014, it’s not expected to be complete until 2029. src

*

In 2009, the Department of Transportation published a strategic plan for US high-speed rail development, which designated 10 high-speed corridors.

Note: The plan does not include a specific timeline for completion of the high-speed corridors.

src:

US Department of Transportation. April 2009.

“High-Speed Rail Strategic Plan.” P.6

Transportation: General Transit and Cars

Summary

This collection of data includes the following indicators:

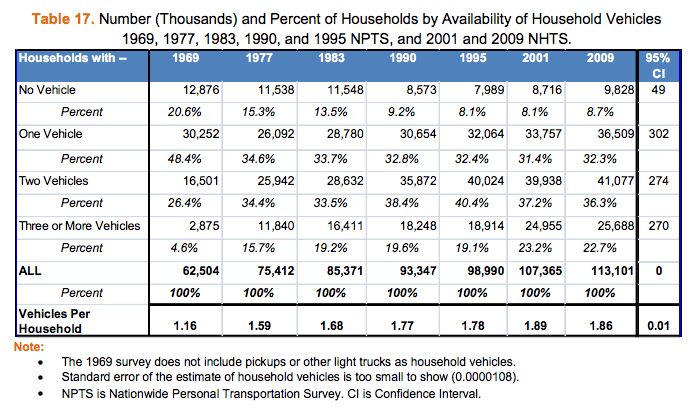

vehicles per household, 1969-2009, Dept. of Transportation

licensed drivers per household, 1969-2009, Dept. of Transportation

vehicles per licensed driver, 1969-2009, Dept. of Transportation

vehicles per worker, 1969-2009, Dept. of Transportation

daily person trips, 1969-2009, Dept. of Transportation

daily person miles of travel (PMT), 1969-2009, Dept. of Transportation

daily vehicle trips, 1969-2009, Dept. of Transportation

daily vehicle miles of travel (VMT), 1969-2009, Dept. of Transportation

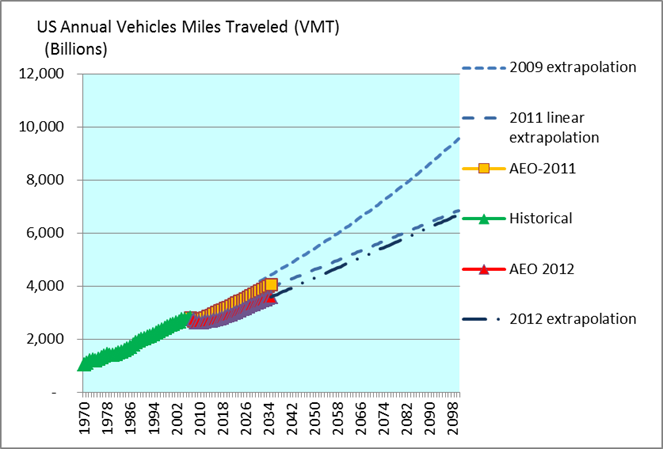

total annual VMT, 1994-2032 & 2014-2044 & 1970-2098, Dept. of Transportation (Frontier Group), Thomas

total annual VMT for light-duty vehicles (LDV), 2014-2040, US Energy Information Administration (EIA)

average person trip length (miles), 1969-2009, Dept. of Transportation

average vehicle trip length (miles, 1969-2009, Dept. of Transportation

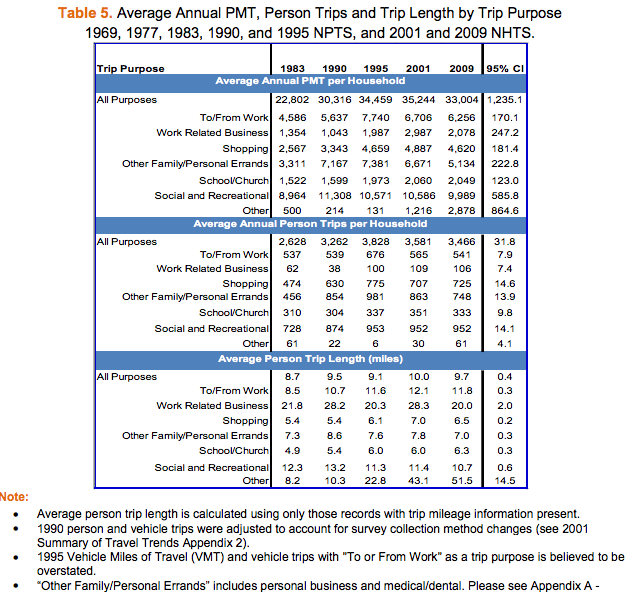

avg annual PMT/household by purpose, 1983-2009, Dept. of Transportation

avg annual person trips/household by purpose, 1983-2009, Dept. of Transportation

avg person trip length (miles) by purpose, 1983-2009, Dept. of Transportation

availability of household vehicles, 1969-2009, Dept. of Transportation

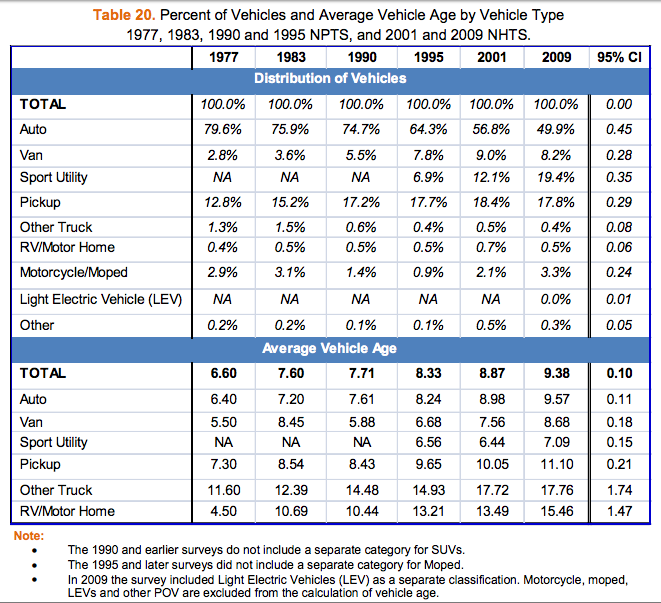

vehicle prevalence by age and type, 1977-2009, Dept. of Transportation

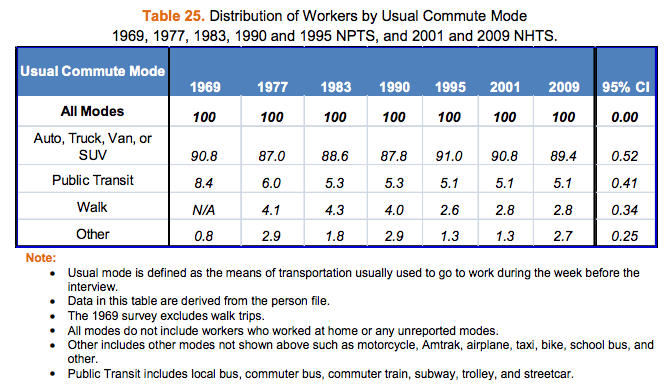

distribution of workers by commute mode, 1969-2009, Dept. of Transportation

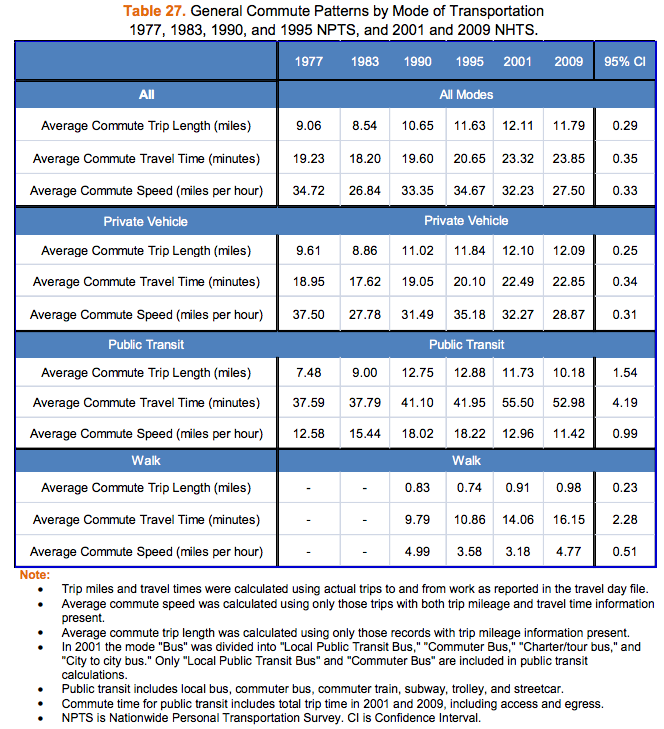

commute patterns by mode of transportation, 1977-2009, Dept. of Transportation

avg commute time to work, 1980-2013 & 2005-2014, Census Bureau

Chicago metro commute, 2000-2030, Alex Anas

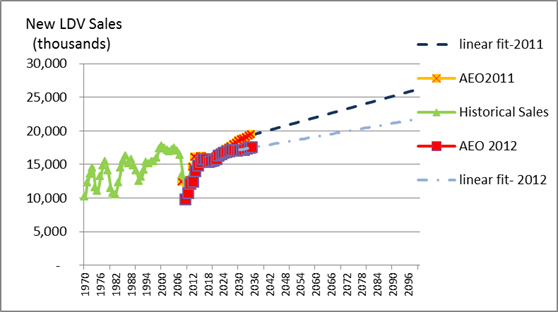

LDV sales, 2014-2040 & 1970-2100, EIA, Thomas

vehicle production vs. car sharing, 2015-2030, Morgan Stanley

Alternative-fuel cars sales, 2014-2040 & 2000-2050 EIA, Nat’l Research Council

autonomous vehicle sales, –2035 & 2014-2036 & –2040 IHS, BCG, Jiang, IEEE

autonomous vehicle dev timeline, 2015-2030, PwC

Findings

General

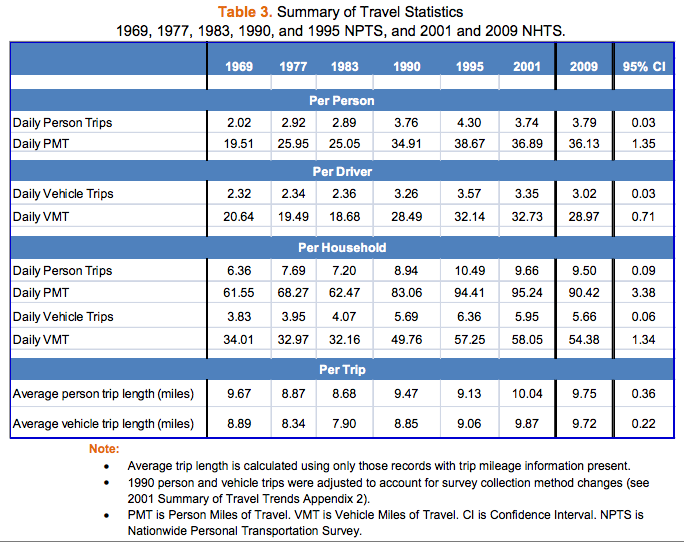

The Department of Transportation has been collecting data about daily personal travel patterns via two different, periodic surveys going back to 1969. Subsequent survey years have been: 1977, 1983, 1990, 1995, 2001, 2009, and 2016 (underway).

Abstract:

The 2009 National Household Travel Survey (NHTS) provides data to characterize daily personal travel patterns across the country. The survey includes demographic data on households, vehicles, people, and detailed information on daily travel by all modes of transportation. NHTS survey data is collected from a sample of households and expanded to provide national estimates of trips and miles of travel by travel mode, trip purpose, and other household attributes. When combined with historical data from the 1969, 1977, 1983,1990, and 1995 NPTS and the 2001 NHTS, the 2009 NHTS serves as a rich source of detailed travel data over time for users. This document highlights travel trends and commuting patterns in eight key areas – summary of travel and demographics, household travel, person travel, private vehicle travel, vehicle availability and usage, commute travel patterns, temporal distribution, and special populations.

src:

A. Santos, et al. 2011.

“Summary Of Travel Trends: 2009 National Household Travel

Survey.”

U.S. Department of Transportation.

NOTE: 2016 SURVEY IS UNDERWAY

*

The Bureau of Transportation Statistics publishes historic data on annual passenger-miles in aggregate, broken down by method of transportation. The chart currently shows data from 1960-2014.

Src:

Department of Transportation. Bureau of Transportation Statistics. Accessed November 8, 2016.

“Table 1-40: U.S. Passenger-Miles (Millions).”

XLS

TO DO: EXTRACT DATA

Commute

The Census Bureau (in addition to the Dept. of Transportation) has asked survey questions about daily travel patterns going back to 1980 (and back to 1960 for a couple of very specific questions). Questions have been asked during the decennial census (since 1980, maybe 1960), and during the “American Community Survey” (going back to 2005).

src:

Beth Jarosz and Rachel T. Cortes. September 2014.

“In U.S., New Data Show Longer, More Sedentary Commutes.”

Population Reference Bureau.

citing:

U.S. Census Bureau, Decennial Census 1960, 1970, 1980, 1990, 2000, and American Community Survey 2013.

Mean Travel Time to Work (minutes)

2005 – 25.1

2006 – 25.0

2007 – 25.3

2008 – 25.5

2009 – 25.1

2010 – 25.3

2011 – 25.5

2012 – 25.7

2013 – 25.8

2014 – 26.0

src:

United States Census Bureau. 2005-2014.

“American Community Survey.” Table S0802: Means of Transportation to Work by Selected Characteristics.

links above

*

This article presents data and extrapolations explaining why urban commute times have not increased more dramatically, despite decades of urban sprawl.

One study (Alex Anas, SUNY Buffalo) extrapolates commute times for the Chicago metro area from 2000 to 2030. In that time, there is a 24% jump in population, leading to 19% more urbanized land (sprawl), but only a 4.5% rise in commute time (from 30 minutes to 31.7 minutes).

Another study (MIT Senseable City Lab) examines cell phone data to track commutes around the world. The study finds travel time, on average across the world, to be largely independent of distance.

The article says that these studies seems to support the theory of “travel time budgets,” developed first by Yacov Zahavi and further by Cesar Marchetti (that travel budgets have averaged about an hour throughout history, and across the world). Both studies seem to support the idea that people adapt their lifestyles to accommodate an average travel time budget, whether by changing mode of transportation (e.g.: switching to public transportation), moving closer to their jobs, or reducing trips that aren’t commutes.

src:

Eric Jaffe. June 2014.

“Why Commute Times Don’t Change Much Even as a City Grows.”

The Atlantic: CityLab

More information about Anas’ extrapolation model, which includes several complex indicators, can be found on this page at his personal website:

“The RELU-TRAN Model and its applications”

TO-DO: ANAS’ MODEL MAY BE IN THE PROCESS OF BEING APPLIED TO LOS ANGELES AND OTHER METROS. INQUIRE ABOUT GENERALIZATION TO THE US.

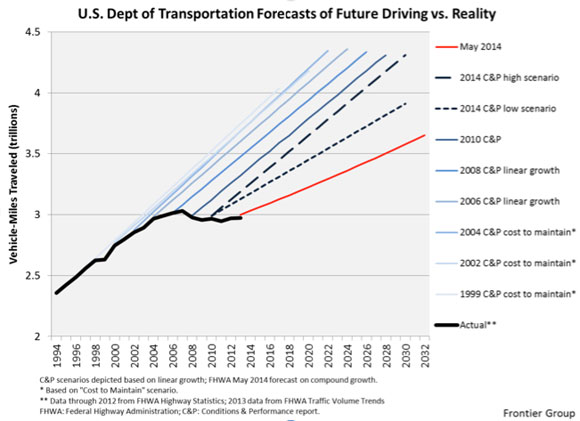

Total Vehicle Miles Traveled

The new report’s 30-year estimates predict even less rapid growth in driving, forecasting that total driving miles will increase only 0.75 percent annually from 2012 to 2042. With population growth estimated to average 0.7 percent each year, this leaves per-person driving miles essentially flat. “This represents a significant slowdown from the growth in total VMT experienced over the past 30 years, which averaged 2.08% annually,” says the report.

src:

Phineas Baxandall. January 2015.

“The Feds Quietly Acknowledge the Driving Boom Is Over.”

StreesBlogUSA.

citing:

Federal Highway Administration. May 2014.

“FHWA Forecasts of Vehicle Miles Traveled (VMT): May 2014.”

and:

U.S. PIRG/Frontier Group (graphic src)

*

The Federal Highway Administration’s spring 2016 forecast revises the growth outlook even further downward.

Excerpt:

Growth in total VMT by all vehicle types is projected to average 0.92% annually over the next 20 years (2014-2034). Over the entire 30-year forecast period (2014-2044) the average annual growth rate is projected to be 0.61% annually, as growth is projected to slow to 0.30% annually during the last decade (2034-2044). This outlook represents a significant slowdown from the growth experienced over the past 30 years, when growth in total VMT averaged 2% annually, although more detailed analysis shows that growth in overall motor vehicle travel per Capita was already slowing throughout most of that period.

[Emphasis mine]

src:

Federal Highway Administration. May 2016.

“FHWA Forecasts of Vehicle Miles Traveled (VMT): Spring 2016.”

Department of Transportation.

*

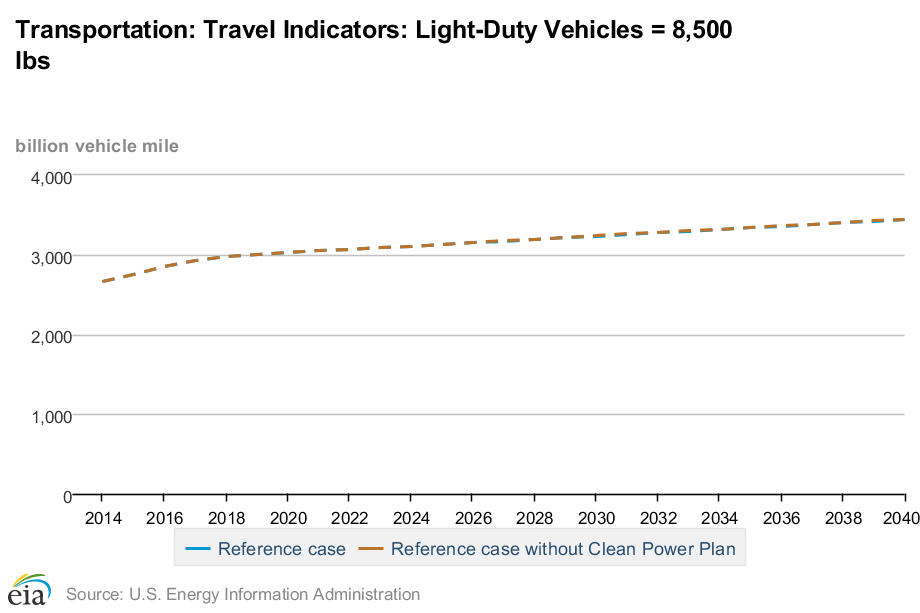

Transportation: Travel Indicators: Light-Duty Vehicles = 8,500 lbs

Visit the source URL for data (many export options).

src:

US Energy Information Administration. 2016.

“Annual Energy Outlook 2016”

Transportation Sector

Table: Light-Duty Vehicle Energy Consumption by Technology Type and Fuel Type

NOTE: ONLY THE DATA TABLES ARE CURRENTLY AVAILABLE. THE EXECUTIVE SUMMARY AND OTHER NARRATIVE PARTS OF THE REPORT WILL BE AVAILABLE AFTER JULY 21, 2016. CHECK BACK HERE.

*

The National Hydrogen Association created a few projections of US Annual Vehicle Miles Traveled (VMT) between 2007 and 2012. Their model performs a linear extrapolation from the EIA’s Annual Energy Outlook (AEO) for 2012, which projects VMT through 2023. Their extrapolation goes through the end of the 21st century. (Results are published at the lead author’s website, “Alternative Vehicles”.)

src:

C.E. Thomas. 2013.

“LDV VMT & Sales.” Alternative Vehicles.

contact: thomas@cleancaroptions.com, faq@cleancaroptions.com

TO DO: CONTACT DR. C.E. (SANDY) THOMAS TO ASK IF THERE HAS BEEN A RECENT UPDATE.

LDV Sales Projection

Light-Duty Vehicle Sales: Total Sales, Cars and Light Trucks

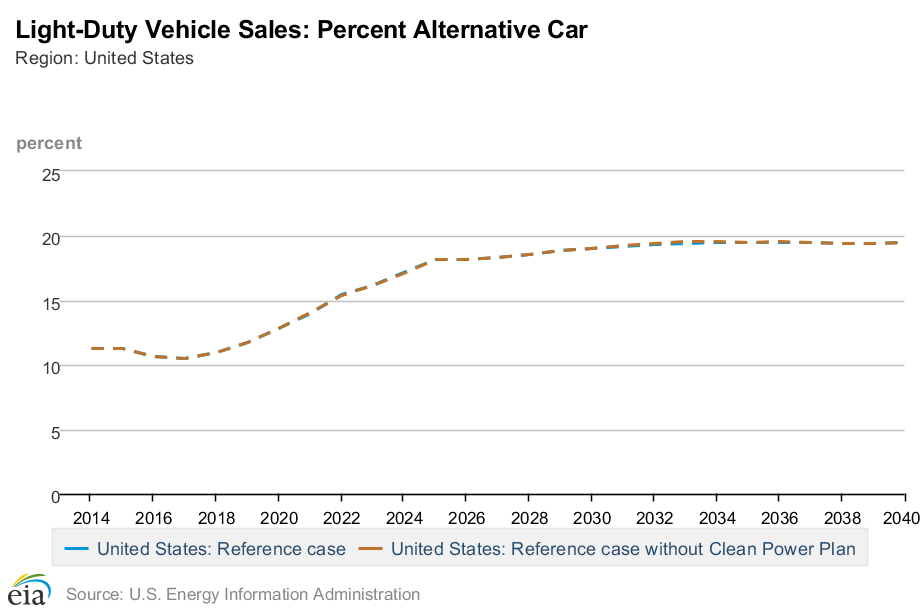

Light-Duty Vehicle Sales: Percent Alternative Cars

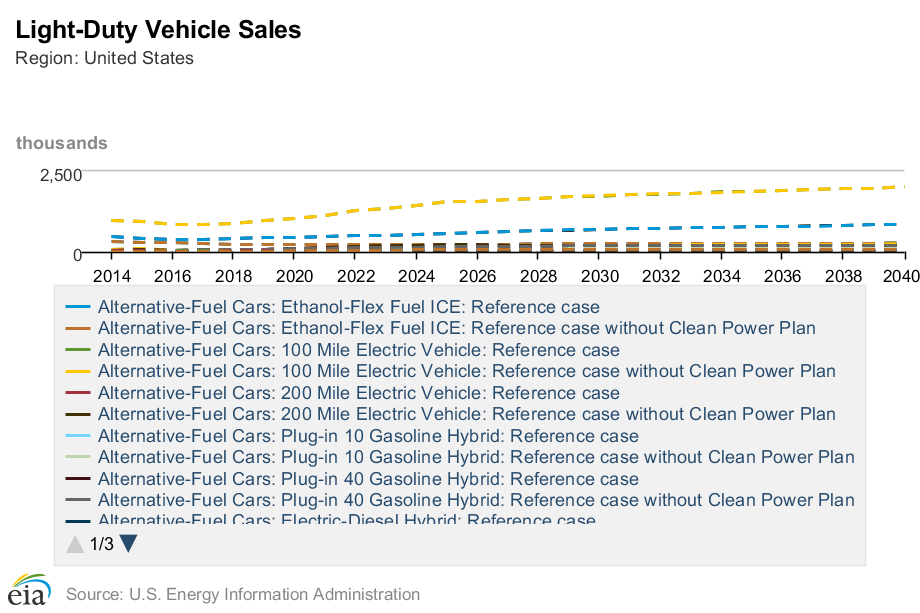

Light-Duty Vehicle Sales: Alternative-Fuel Cars

Visit the source URL for data (many export options).

src:

US Energy Information Administration. 2016.

“Annual Energy Outlook 2016”

Transportation Sector

Table: Light-Duty Vehicle Energy Consumption by Technology Type and Fuel Type

*

src:

C.E. Thomas. 2013.

“LDV VMT & Sales.” Alternative Vehicles.

contact: thomas@cleancaroptions.com, faq@cleancaroptions.com

TO DO: CONTACT DR. C.E. (SANDY) THOMAS TO ASK IF THERE HAS BEEN A RECENT UPDATE.

*

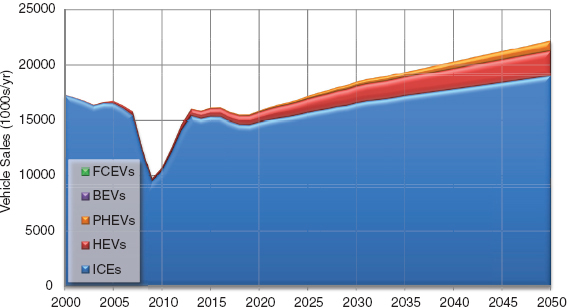

5.3.1 Baseline Cases

Excerpt:

In the [business as usual] case, new-vehicle sales increase to 22.2 million in 2050 from 10.8 million units in 2010 (a year in which sales were severely depressed due to the recession). Diesel, hybrid, and plug-in hybrid vehicles make modest gains in market share (Figure 5.1). The total stock of LDVs increases from about 220 million in 2010 to 365 million in 2050.

FIGURE 5.1 Vehicle sales by vehicle technology for the business as usual scenario.

FCEVs: fuel cell electric vehicles

BEVs: battery electric vehicles

PHEVs: plug-in hybrid electric vehicles

HEVs: hybrid electric vehicles

ICEs: internal combustion engines

Note: In this model total new car sales and annual vehicle miles traveled (VMT) are assumed to be the same as in the projections from the Annual Energy Outlook 2011

src:

National Research Council. 2013.

Transitions to Alternative Vehicles and Fuels.

Chapter: 5 Modeling the Transition to Alternative Vehicles and Fuels.

The National Academies Press.

*

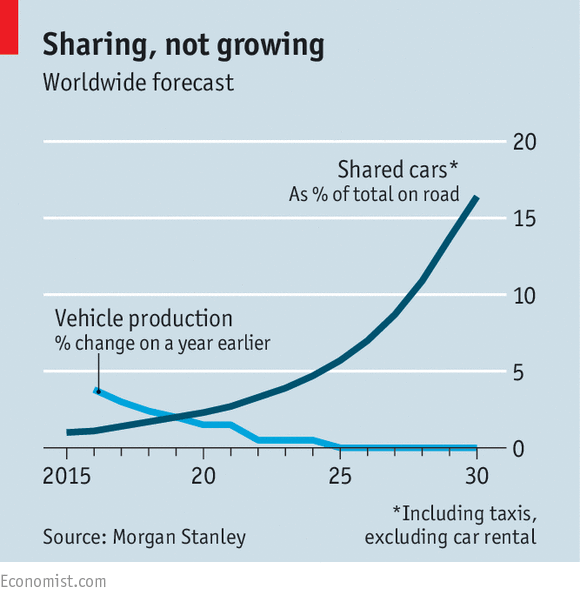

Production Vs. Sharing

Src:

The Economist. January 2016.

“The driverless, car-sharing road ahead.”

Autonomous Vehicle Sales

IHS forecasts 76 million autonomous vehicles will have been sold globally through 2035, with 21 million of those being sold that year.

“The U.S. market is expected to see the earliest deployment of autonomous vehicles as it works through challenges posed by regulation, liability and consumer acceptance. Deployment in the U.S. will begin with several thousand autonomous vehicles sold in 2020, which will grow to nearly 4.5 million vehicles sold in 2035, according to IHS Automotive forecasts. As in many other markets, a variety of use cases and business models are expected to develop around consumer demand for personal mobility.”

IHS expects a global CAGR of 43% between 2025 and 2035.

src:

IHS. June 2016.

“CORRECTING and REPLACING IHS Clarifies Autonomous Vehicle Sales Forecast – Expects 21 Million Sales Globally in the Year 2035 and Nearly 76 Million Sold Globally Through 2035.”

contacts:

Michelle Culver michelle.culver@ihs.com

press@ihs.com

TO DO: ASK IF THEY CAN SHARE ANNUAL DATA POINTS.

*

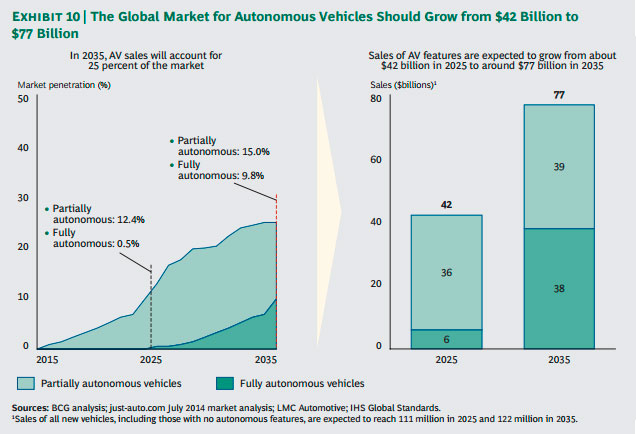

“In 2035, AV sales will account for 25% of the market.”

src:

Boston Consulting Group. April 2015.

“Revolution in the Driver’s Seat.”

P.18

Note: The report uses expectations for the U.S. as an accurate proxy for the global market-penetration. This is based on adoption rates in the U.S. for adaptive cruise control being in line with overall global adoption.

*

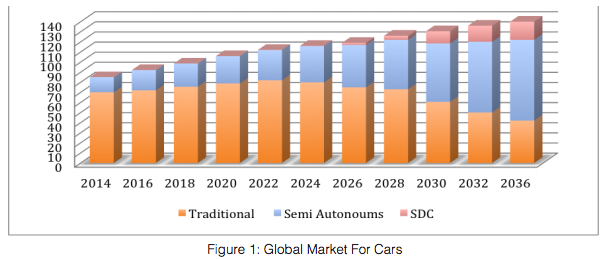

Cars sold globally 2014-2036

2014 – total 90M+, autonomous or self-driving 15M+

2030 – 50% autonomous or self-driving

src:

Tao Jiang et al. 2015

“Self-Driving Cars: Disruptive or Incremental?”

Applied Innovation Review, 1. P.6

NOTE: The authors are from Google, Samsung, Yahoo, and Altera, but the data above is not sourced.

TO DO: CONFIRM SOURCES FOR ABOVE DATA. (HAVEN’T BEEN ABLE TO FIND EMAIL ADDRESSES FOR ANY OF THE AUTHORS – MIGHT HAVE TO REACH OUT VIA LINKEDIN, OR THE JOURNAL’S EDITORS.)

*

In 2012, IEEE said that it expected autonomous vehicles to account for up to 75% of cars on the road (globally) by 2040.

TO DO: TRACE THE SOURCE. POSSIBLY ALBERTO BROGGI, UNIV. PARMA, ITALY.

src:

IEEE. September 2012.

“Look Ma, No Hands!”

IEEE News Releases

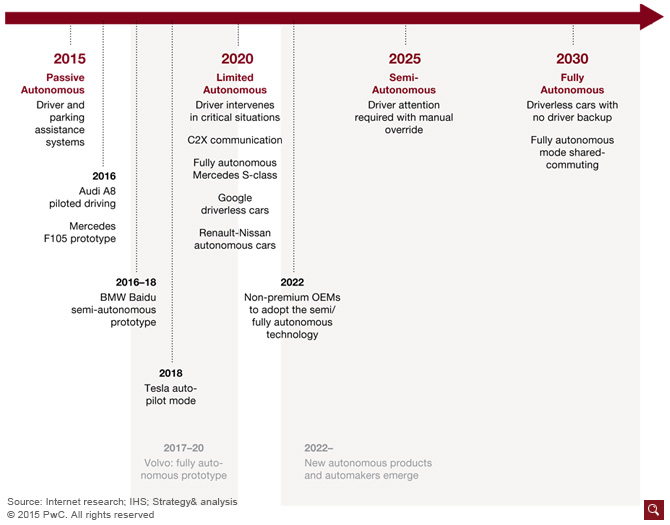

Autonomous Vehicle Development Timeline

Exhibit 7: Possible time line of autonomous car innovation

src:

Richard Viereckl et al. September 2015.

“Connected Car Study 2015: Racing ahead with autonomous cars and digital innovation.”

Strategy&. PwC.

NOTE: Although this paper is focused on the European Union, I believe this timeline is general to the industry as a whole.